In today’s blog post, we’ll be completely dismantling an asinine article published this week by Allison Morrow and Anneken Tappe for CNN Business. The article, titled “Why inflation can actually be good for everyday Americans and bad for rich people,” attempts to make the case that inflation is actually a “good thing” for wage earners and middle-class Americans and hurtful to “rich people.” At best, it’s looking at the economy through rose-colored glasses. At worst, it’s a dangerous propaganda piece covering for an administration currently struggling with the inflation demon.

This counterpunch to an article might turn out to be a new format. Coincidentally, I was halfway through a blog post on protecting one’s self from inflation when Morrow’s article was published two days ago. I had to stop and comment on possibly the dumbest article I’ve ever seen put out by the mainstream media.

Without further ado, let’s dive in.

Claim: Wages are going up, “empowering workers”

inflation can actually be a good thing for many working-class Americans, especially those with fixed-rate debt like a 30-year mortgage. That’s because wages are going up, which not only empowers workers but also gives them more money to pay down debt.

The article is correct in that wages are indeed going up. However, real earnings, or wage increases versus inflation, is negative. The U.S. Bureau of Labor Statistics (BLS) reported that real earnings in October 2021 decreased half a percent, a result of “an increase of 0.4 percent in average hourly earnings combined with an increase of 0.9 percent in the Consumer Price Index for All Urban Consumers.”

This means that although wages increased…inflation increased more, resulting in a net loss of purchasing power. Put another way, wages aren’t keeping pace with inflation on average. How can one be empowered to pay down debt when they’re losing the race against the price of everyday items? (The CPI doesn’t even include energy prices, but I digress…)

In fact, real wages have been negative since April.

“For now, inflation is going to continue to run above very solid wage growth,” said Joseph LaVorgna, chief economist for the Americas at Natixis and former chief economist for the National Economic Council during the Trump administration. “This is why when you look at consumer confidence, it’s really taking a beating. Households do not like the inflation story, and rightly so.”

Response: Workers are not empowered. Wages are losing against inflation.

Claim: Inflation gives homeowners a ‘discount’

Meanwhile, wages are rising along with prices, essentially shrinking the real value of that debt. The same inflation benefit applies to anyone paying off federal student loans, which also have a fixed interest rate. As your income increases, you’re essentially getting a discount on what you have to repay.

The article discusses how working class Americans get a ‘discount’ on their mortgage, as inflation drives up the price of their home, but the fixed-rate mortgage payments and interest rate remain stagnant. If your home increases from $150,000 to $200,000 due to inflation but your mortgage is only for the $150,000 — you made out.

Except not really. Yes, your financial balance sheet is improved by the home value increasing and the debt-to-equity ratio tipping in your favor, but costs associate with the home climb with inflation. Your utility bills like electricity and water will increase. As inflation drives up the costs for local governments and school systems, your property taxes will also increase. Most people pay their local and school taxes out of their monthly mortgage payment, which will rise in conjunction. Expect homeowners insurance to rise accordingly, feeding into an increased monthly payment.

And then there’s the cost of home repairs. Lumber prices alone are up 124% since August 2021. Inflation on materials could wipe out any minuscule gains made against your mortgage payment.

Do you know who doesn’t suffer against increases to their property taxes and utilities? The rich. The same group CNN’s article claims will be hurt by inflation. Why is this? Many wealthy people own rental properties. In a rental property, you can raise rent to keep up with inflation. Utilities and property taxes are business deductions, so the more they increase the more the property owner can write off against the cash flow generated.

Response: The debt-to-equity ratio on paper looks better due to inflation, but homeowners will ultimately suffer more. Ironically, the group CNN claims will be hurt by inflation is actually protected against it with owning rental properties.

Claim: The rich will be hurt by their bond holdings

“Who are the ones that are going to be hurt by holding a lot of 10-year bonds or even 30-year bonds? That tends to be higher-income households, says Smetters. “So they’re going to lose with higher inflation.”

The lone argument for why inflation “hurts rich people” — stated boldly in the article headline — is that “households with more than $1 million who typically invest in both equities and debt” will be crushed by inflation because of their government bond holdings.

You don’t become rich by investing in stupid things. Or better yet, you don’t stay rich by holding dumb investments. Bonds are a terrible investment in inflationary periods. They are fixed instruments, like the fixed mortgages mentioned above. Worse over, the interest rates paid by bonds like U.S. Treasuries generally offer negative real rates against inflation. The article fails to identify or even give an example of these $1 million households that are holding bonds.

Do you know who holds lots of U.S. Treasury bonds? Pension funds and employee retirement plans like 401k and IRAs. An outmoded method to invest for retirement has long been to buy equities (stocks) while young and slowly transition to bonds over time as you near retirement age. This is because stocks can be volatile and you don’t want to face a market crash the same year you planned to retire. By moving to fixed assets like bonds, they don’t really move up or down and they pay interest — good for generating cash after you’ve retired.

You may have heard of Target Date Funds. These are financial vehicles offered by all the retirement plans and company-sponsored 401ks. It essentially does the above mentioned retirement migration from stocks to bonds for you (for heavy fees, of course). So when you go to finally retire at age 65, your portfolio is jam-packed with U.S. Treasuries that are losing value against inflation and paying you monthly interest below the CPI.

Morrow’s CNN article even admitted as much further down: “And anyone living on a fixed income, such as retirees, who aren’t benefiting from wage increases that people in the labor force are seeing, are feeling extra pain as prices go up.”

Response: The bond holders that will be severely hurt by inflation are the wage earners and working class that busted their hump for 40 years only to see their retirement accounts shrink against inflation. And these are the people who retire and must live off these accounts they spent 40 years prepping. Many pension plans are also forced to hold U.S. Treasuries as they’re deemed ‘safe’ investments and non-volatile.

The rich can sell off their bad holdings and buy something else. Or the gains made in other assets like real estate, stocks, (or even tangibles like artwork), far out gain losses to treasury bonds.

In conclusion, this CNN article is a mess. Inflation is never a ‘good’ thing. It’s morally unjust, eating away at stored productivity and savings. It consumes the lower class, pushing prices up beyond the reach for many things. There is nothing good about inflation to the working class. There is a reason inflation is called a “stealth tax.”

I’ll end my rebuttal with George Gobel’s famous words: “If inflation continues to soar, you’re going to have to work like a dog just to live like one.”

From the very beginning of this blog, I’ve stated an emergency fund is critical in life. It’s also certainly not just me: Dave Ramsey preaches it; every financial advisor advocates for it. The very first step in my being able to quit my job was having an emergency fund. I’ve mentioned it repeatedly in past blog posts, so why bring it up again?

Because I just had to spend nearly all of mine.

It’s one thing to have an emergency fund — that cash set aside in case life intervenes — and sleeping easy at night knowing you’re prepared for what might come the next day. It’s another thing to watch it drain out over the course of a few weeks. Over the past six months, I had bulked my emergency fund up to cover six full months of expenses in case something happened to my wife’s job or my business. There was no need to panic, it was just good financial sense.

So what happened?

In early March, I had a simple medical procedure done as a prevention measure. My mother was diagnosed with cancer in her mid-40s, so me in my late 30s have been pressured by my doctor to have some preventative testing done. As it turns out, the procedure is not covered by my insurance (because they deem me “too young” to have the testing done — even though it could save them millions in the future). Bill #1 was over $1,340.

This year was my first year of paying quarterly taxes. When you own your own business and you’re not on a payroll, it’s common practice (and the IRS can issue penalties if you don’t) to do a mini-tax return every 3 months and mail in your own withholding. So April 2021 was my first quarter 2021 taxes (January – March). Fine, I was prepared for that. What I wasn’t so prepared for was my CPA discovered my previous 2019 tax return wasn’t filed properly by my former CPA, and there was significant back taxes and interest owed because of it. Bill #2 was $8,100.

This month 2020 taxes were due. The number was slightly higher than anticipated, and my tax savings account decimated by the 2019 taxes, so I had to pull from my emergency fund to cover the shortfall. Bill #3 was $2,200.

Three tax hits in a row and a medical bill. I had gone four rounds with Murphy’s Law and could get back up. But Murphy wasn’t done.

Last week not one, but two major appliances in my house went. My LG refrigerator (do not ever buy a LG fridge) had the compressor go and has slowly been getting warmer and ruining the food in the freezer and fridge. My washing machine had its motor burn out. Bill #4 and #5 were $2,400.

That’s over $14,000 in 60 days that had to be covered. Imagine if I hadn’t had an emergency fund to draw from? Or if I hadn’t decided to beef up to 6 months of expenses saved — it would have been life altering. I would have had to go into debt to cover the medical costs and appliances, making payments and paying interest. Even worse, the IRS does not take credit card. Taxes must be paid in cash. If I hadn’t had the emergency savings to pay all the taxes, the IRS would have set up an installment plan — with more penalties and fees — and I’d have to pay them back monthly for years.

This is why you need, NEED, NEED, NEED an emergency fund.

So my six months of expenses is exhausted. What now? The process restarts. I will set aside money to ‘regrow’ the emergency fund. Life always regroups and will come around again. You can keep Murphy at bay, but he’s never truly gone. I will set aside what I can each month to rebuild, and given the extent of these past two months, I have resolved to save beyond six months expenses. Maybe a year this time?

If you plan to quit your job and build your life, you can’t do it without an emergency fund. If you have an emergency fund, let this post inspire you to add a little extra to it! Life strikes randomly. Things happen. We can’t plan for everything or know everything, but we can do is be prepared.

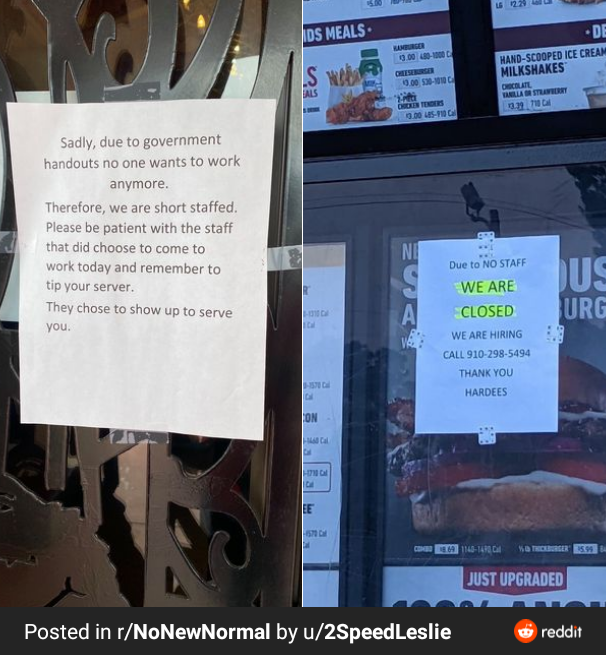

The unthinkable has happened. Millions of Americans have embraced freedom from work and have now reclaimed their lives from the dreaded grind of employment. So many have walked away that businesses can’t fill job openings. We did it! Freedom is in the air and so many people have the opportunity now to build that business, find that calling, or go bohemian.

There’s no longer a need for a blog called “Quit Your Job” these days. It’s already been done.

But back to reality. While the above sounds utopian, that’s not what is going on exactly. At the moment, unemployment is high…but companies are also struggling to hire anybody. A recent article from the New York Timestitled “Unemployment is High. Why Are Businesses Struggling to Hire?” lays it out:

“…the data tables produced every month by the Bureau of Labor Statistics, which suggest a plentiful supply of would-be workers. The unemployment rate is 6 percent, representing 9.7 million Americans who say they are actively looking for work…[while] businesses, especially in the restaurant and other service industries, say they face a potentially catastrophic inability to hire.”

So we’ve got jobs and people looking for jobs, yet the jobs remain unfilled and the people remain unemployed. What gives? Recently, a McDonald’s in Florida is offering people $50just to come in to interview for a job because they’re so short staffed and unable to hire. You read that correctly. McDonald’s — once the employer used as a threat for people who didn’t want to go to school or study (as in “You’ll end up working at McDonald’s”) — can’t even hire right now. McDonald’s is also offering a $400 signing bonus if you end up getting the job. The state of Montana is bribing citizens with $1,200 if they go back to work, “blaming an expansion of unemployment benefits for a labor shortage in the state.”

Now states are reopening up, restrictions easing off, and businesses trying to return to normal. But the workers aren’t coming back. Is it because of COVID fears and aversion to risk being around people? Maybe that’s part of it. According to the Chicago Tribune, “A Census survey taken in late March shows that 6.3 million didn’t seek work because they had to care for a child, and 4.1 million said they feared contracting or spreading the virus.”

There’s also something else at work here. From the same Chicago Tribune article, entitled “Where Are the Workers?”:

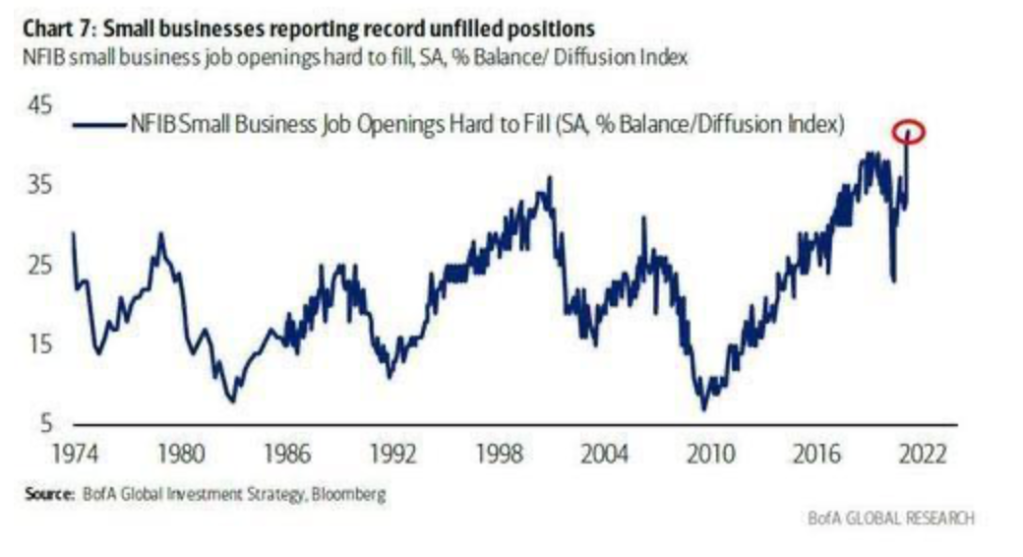

The National Federation of Independent Business found in a March survey of its own members that 42% had job openings they couldn’t fill. Owners cited higher unemployment benefits as one factor. And a study released last month by the National Bureau of Economic Research found that a 10% increase in unemployment benefits during the pandemic led to a 3.6% drop in job applications.

“Unemployment benefits allow workers to be able to wait longer before they take a job, which can make hiring harder,” said Ioana Marinescu, a University of Pennsylvania professor who co-authored the study.”

Unemployment benefits, particularly Federal ones, have caused disruptions in the labor market. A ZeroHedge article, “Biden’s Trillions” Spark Historic Labor Shortage” puts it [perhaps oversimplified] as “trillions in Biden stimulus are now incentivizing potential workers not to seek gainful employment, but to sit back and collect the next stimmy check for doing absolutely nothing in what is becoming the world’s greatest “under the radar” experiment in Universal Basic Income.”

Universal Basic Income (or UBI) is an eventual topic I plan to cover in this blog.

Between DD and McDonald’s, businesses are literally bribing people to come work for them. Gone are the days, it seems, where winning a job and earning an income were admirable achievements. I guess it comes down to if you can make $900 a week working a job, or $800 not leaving the house…why not take the $800? You don’t have to drive anywhere, do anything, change clothes, or actively participate in society.

Which makes having a blog called “Quit Your Job” all the more abstract.

So government altruism is disrupting the job market. How long can it go on? Businesses still need employees to function. Not having enough employees is also severely disrupting supply chains, causing shortages and empty shelves. Another article from Zerohedge, this one entitled “Biden’s Stimulus Checks ‘Wreck Labor Pool’ As People Get Paid to Stay Home,” quotes the Federal Reserve Bank of Kansas City: “It is very difficult to handle the increased business with supply chain issues across all materials and finding anyone who wants to work. The federal government has incentivized people to stay home and not be productive.” This, combined with extra cash being handed out by the government, is very inflationary (also a future topic on this blog).

As mentioned above, surely this can’t go on, right? Hopefully not. The Federal unemployment bonuses are scheduled to expire in September of this year. If the Federal unemployment benefits expire, people will be making below what employment would bring in, so it only makes sense to return to work. Employers need it. The supply chain needs it. Then again, if the supply chain disruptions cause shortages prices of things increase, which would offset the extra unemployment and people would need to return to work just to afford basics. The only thing that doesn’t make sense is to leave the Federal unemployment bonuses permanent, especially as the country continues to reopen.

The idea behind this blog and “Quit Your Job” is to build something — a business, skills, expertise, ultimately bettering yourself so you no longer need to work for someone else. Taking money from the government and choosing not to work is not bettering yourself. Choosing to do nothing over working is not in the essence of Quitting Your Job.

Just remember, there’s no such thing as a free lunch.

In The Big Short, there’s a scene where Michael Burry (Christian Bale) is confronted by two of his biggest clients over Burry’s claim of a housing bubble. The first client, Lawrence, tells Burry that “actually, no one can see a bubble. That’s what makes it a bubble.” Burry responds: “That’s dumb…there’s always markers.”

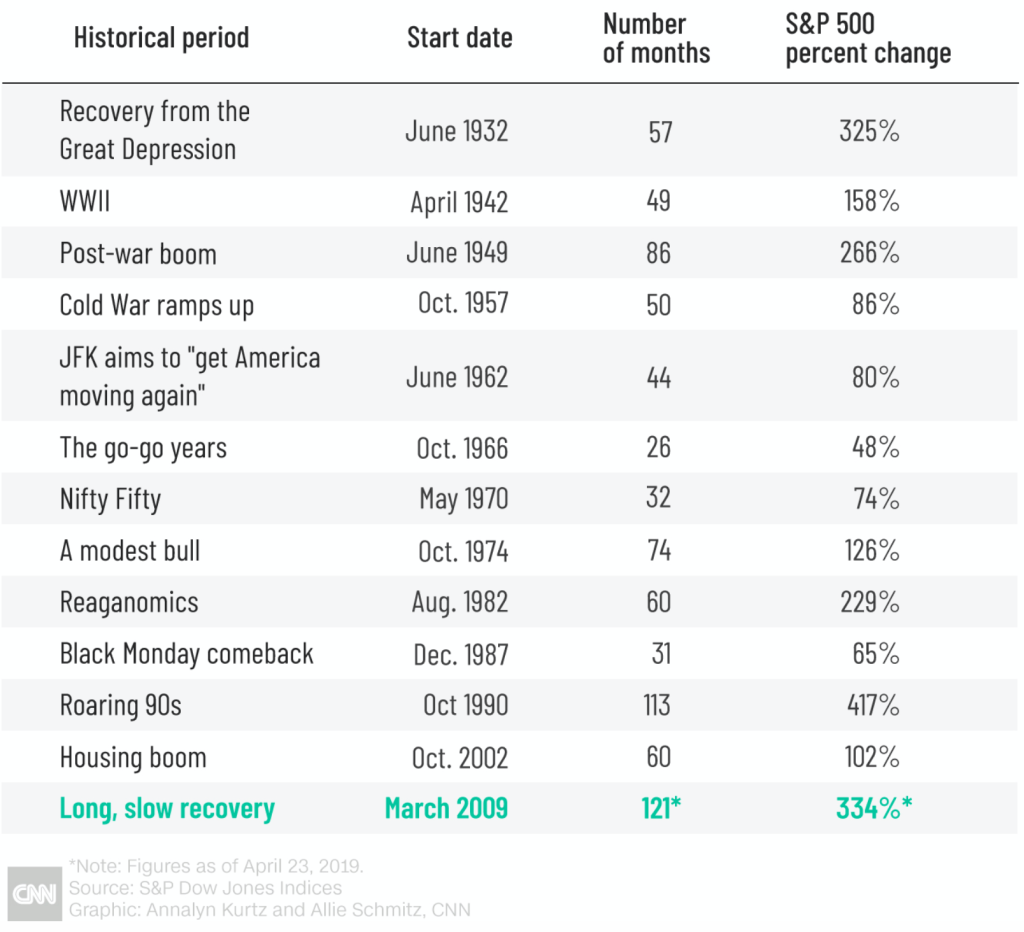

It’s true. There are always indicators, as history has shown. We are currently in the midst of the longest running bull market in history, going all the way back to March 9, 2009. Last February began a large, COVID-induced selloff that corrected course by summer and actually put the market in the green by the end of the year. It was the first time ever a market dropped by 30% and ended green in the same year.

So are we on the verge of the next “Big One?” Here’s five reasons that say we are.

1. Wrong Side of History

As mentioned, we are currently in the longest running bull market of all time. Prior to the 2009-to-present run, the longest was the 1990s, which ran for 113 months. Our current run is at 143 months. Market commentators called last year’s 30% drop the “end of the bull market” but because it came immediately back and then broke the old high I do not consider it the end of the market run. The correction was hefty, but the long term trend line was not broken.

Looking at the list above, prior to our current run starting in 2009, the average bull market lasted 56.83 months. The current run is nearly three times that. Not only that, but the S&P percent change if you include 2020 and 2021 is up to 437.54% taking out the old record from the Roaring 90s.

Simply put, we’re far overdue for an ending to this bull market.

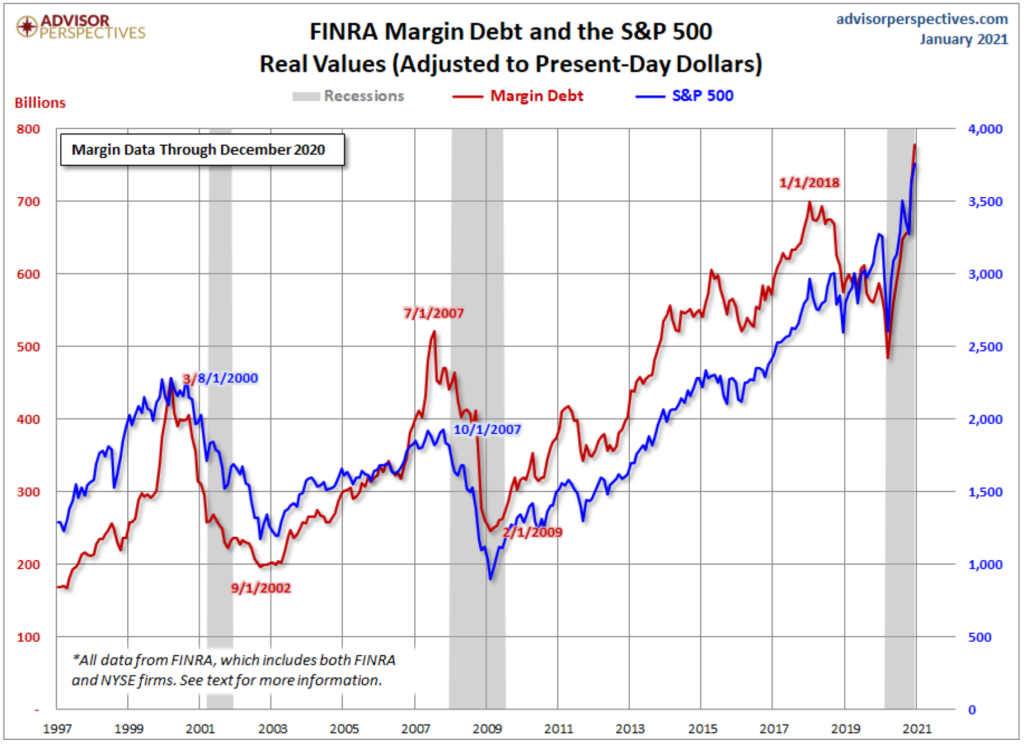

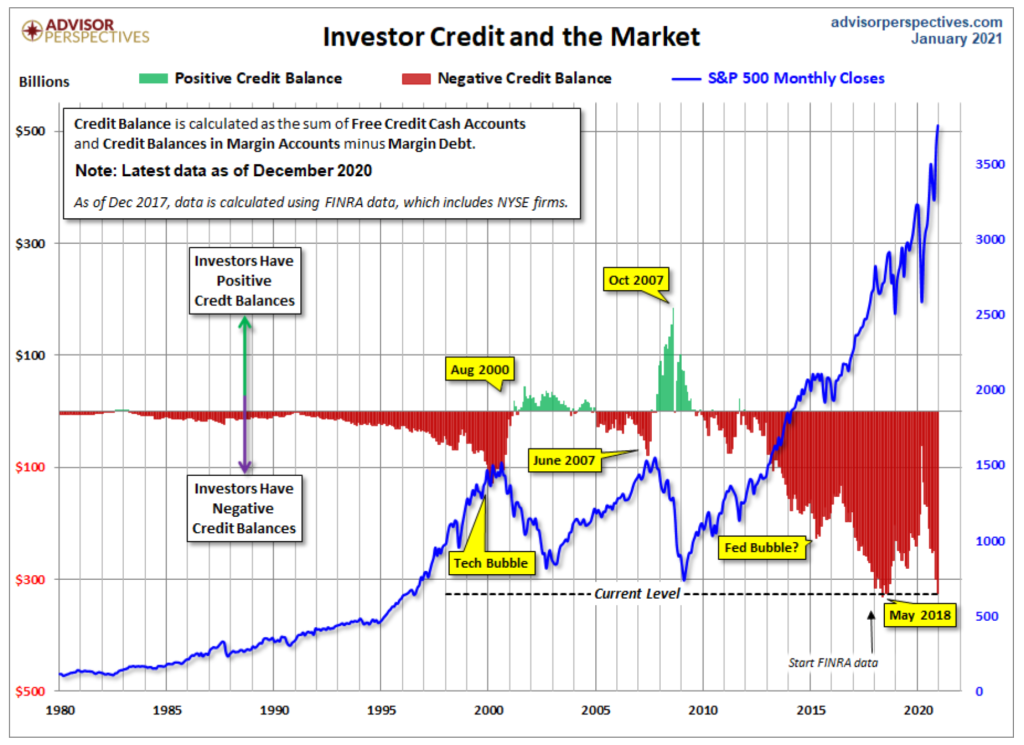

2. Margin Debt is at a Record High

Margin is the difference between the total value of the investment and the amount you borrow from a broker. Basically, you’re using cash or securities you already own as collateral to make more investments in hopes of making a profit. As with other loans, you have to pay back the money you borrowed plus interest. But margin trading comes with risks. If the amount you borrowed gets too large relative to the value of your securities, you will have to deposit more funds. Otherwise, your broker may sell off some of your assets. And remember, even if you lose your entire investment, you’ll still have to repay what you borrowed, with interest.

Website for Robinhood

Any investment bought via credit always runs the risk of margin calls and, eventually, liquidation.

Barry Ritholtz

Margin debt in 2020 reached a record high. Advisor Perspectives has compiled the amount of outstanding margin debt in the S&P 500. The correlation between the amount of debt and the S&P 500 level is not an accident; after all, buying stocks on credit allows you to buy more than you could just on cash alone. By borrowing money from a bank or brokerage to buy stocks (in hopes they go up), funds and investors drive up the market.

The expansion of credit also correlates with past bubbles (and crashes) in the market: the dot com bubble of the late 90s, the housing crash starting in late 2007, and the sharp drawdown in 2020. However, in Jan 2021, the outstanding margin is higher than it’s ever been, lost to the point of going parabolic. The chart below gives a better illustration as to the growing debt burden (or negative credit) overall in the market:

Margin can only expand so far. A bank or brokerage will only lend so much before either the servicing payments or interest becomes too great. There’s also the possibility that a drop in price will precipitate a margin call and the brokerage has the legal power to start selling securities in your account to repay loans. The risk at that point becomes systemic, with multiple brokerages liquidating accounts to get their money back.

For example: I have $100 and I buy 5 shares of AT&T (T). The shares go up in value. I can then use them as collateral to borrow another $100 from my brokerage to buy more shares of T. It goes up, so I borrow another $100 to buy more, and so on. My parents did this during the housing boom in the 2000s: take out a home equity loan to improve the house. The value of the house went up, so the line of credit in the home equity went up, so more could be borrowed for more improvements…and so on. So in my brokerage account, I have over $300 in T stock, only $100 of which was my own money. If T’s stock price drops, the value of the collateral drops, so I get margin called. Worse, if it drops below the price I bought it with my original $100, I could be wiped out. I owe the brokerage $200 regardless, so if all the shares I bought are sold for $200, I have no money left and no shares.

Total wipeout.

Margin debt relies on the “greater fool” theory that pervades every stock market bubble. Essentially, I’m willing to take on the risk of borrowing money to buy stock because I believe there will always be someone (a “greater fool”) to buy it from me. Eventually, there wont be any buyers because prices will reach a point where no one wants (or can) afford a stock. Now you’re stuck with stock quickly losing value that you bought with credit. And if everybody holding that stock tries to sell at the same time or is forced to sell via margin call…well it turns into a landslide.

According to the Financial Industry Regulatory Authority, outstanding margin debt at the end of 2020 was $778.04 billion.

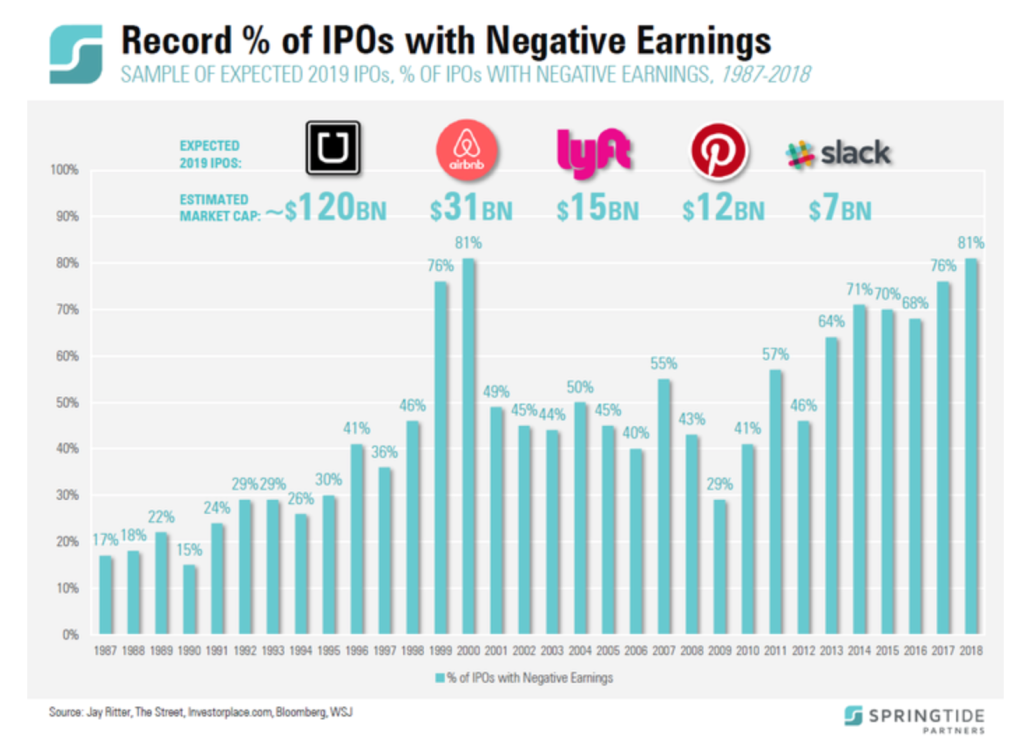

3. Record New IPOs

Jordan Belfort Takes Steve Madden Public in The Wolf of Wall Street (2013)

An Initial Public Offering, or IPO, is when a private company “goes public” by offering shares of the company on the stock market. It is the late stage of start ups: venture capitalists or investors invest money into a company (or person) with an idea, build the company up until it’s functioning and offering a product or service, then sell it via IPO, recouping their investment plus profit. Imagine investing in Apple or Tesla before it went public, then being able to sell off your shares of the company at big returns.

Large amounts of IPOs are also generally seen as a market top or bubble — just look at the dot com craze of the late 90s. Internet startups were dropping shares all over the NASDAQ, with investors desperate to grab anything with “internet” or “dot com” in the name. It eventually became a racket — companies like pets.com that had no real business model or even revenue were being sold to the public.

Defying expectations, investors piled into initial public offerings at a record rate in 2020, and few expect the euphoria to wear off soon.

Companies raised $167.2 billion through 454 offerings on U.S. exchanges this year through Dec. 24, compared with the previous full-year record of $107.9 billion at the height of the dot-com boom in 1999, according to Dealogic.

The coronavirus pandemic turned the typical rhythm of the IPO market on its head, with $67.3 billion raised in the fourth quarter. That amount is roughly six times the total for the first three months of the year.

A lot of this could be driven by retail investors over the course of last year. Axios calls this “The Robinhood effect.” If you recall in my last post titled “Gamestonk,” retail investors (more on them in a minute) dove headfirst into trading stocks using stimulus checks and Federal unemployment bonuses to buy up companies like Tesla.

Even as I write this, the IPO for dating-app Bumble just opened 77% higher than it’s IPO price on its first day of trading. The app disclosed 2.4 million paying users as of September 2020, but also a net loss of $84.1 million…with a net loss margin of 22.3%. With it’s current stock price, the dating app company is valued at $14 billion.

Make no mistake — this is mania. Retail traders are buying shares in IPOs of companies they recognize: AirBnB, Uber, Lyft, Pinterest, and Slack. These are apps and software they know. And they all want to get in on the ground floor in case the stock is the next Tesla or Apple. Just like people didn’t want to miss out on pets.com being the next…well, whatever. Perhaps even more maniacal is the ubiquity of SPACs or “Special Purpose Acquisition Company.” Without going too far down the rabbit hole, here’s The New York Times’s definition: “

These vehicles have only one purpose: to find a private company and buy it, usually within two years. SPACs are sometimes known as “blank check” companies — as in, investors give them a blank check to go buy a business, sight unseen.

Those checks are getting bigger and bigger, with SPACs raising nearly $26 billion in January, a monthly record in an already red-hot market.

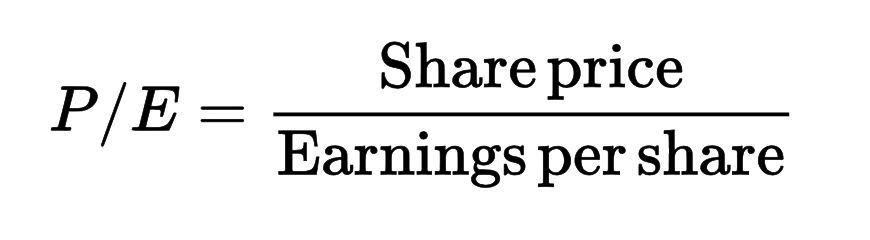

In case you don’t know what a P/E ratio is, I threw out the formula from the get go. More bluntly, it’s the measurement of how far from reality a company’s stock is. If a company that has 1,000,000 shares makes $2,000,000 than its earnings per share (EPS) is $2.00. Now the same company’s stock is $200/share. So $20 divided by $2.00 is a P/E of 10. Therefore, the higher the share price (or lower the earnings per share), the higher the P/E. A P/E of 10 means it would take 10 years to earn back your initial investment through company profits. Another way of looking at it is, people are willing to pay $10 for every $1 a company earns.

This little bit of math is important to understand the impact of a runaway P/E. For the most part, P/E is used as a way to compare valuations between companies. A company with a P/E of 20 might be not be seen as overbought as a company with a P/E of 50. Remember, a P/E of 50 means it would take 50 years to earn back your initial investment through company profits.

Now take a popular stock like Tesla (TSLA), that had a huge run last year due to retail investment interest and cheerleading by ARK’s Cathy Wood. It’s current P/E ratio is 1,268.

If you bought Tesla right now, it would take you over twelve hundred years to earn back your initial investment through Tesla’s profits. Other stocks like Shopify (SHOP) and Square (SQ) have current (as of time of this writing) P/E ratios of 900 and 413, respectively. As a point of reference, a P/E in the mid-20s is traditionally considered “high”. These stocks have become detached from any real financials.

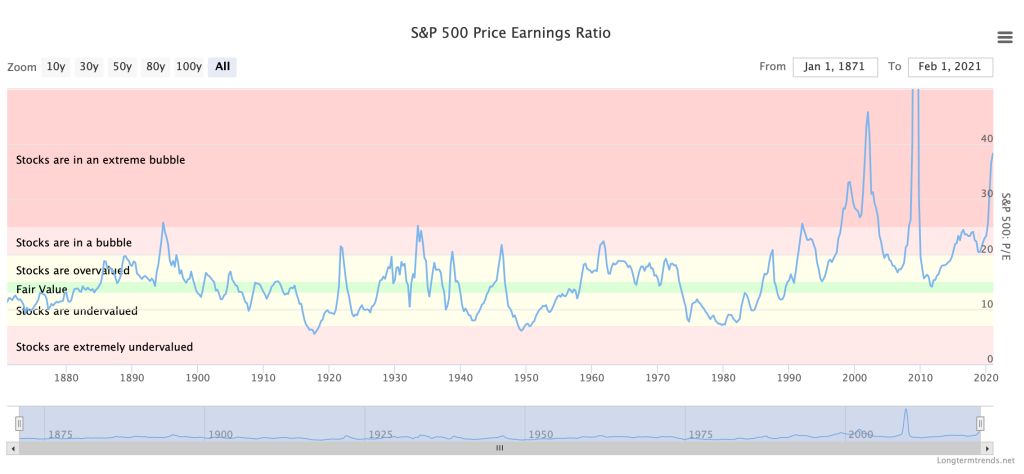

Now expand P/E to the entire stock market, where you aggregate all the companies’ P/E to determine the market P/E. The historical average P/E for the S&P 500 is between 13 and 15. The current P/E for the S&P 500 is 39.87.

For long term P/E analysis, a lot of companies will use something called CAPE — Cyclically Adjusted Price Earnings — or “Shiller PE”. This is the price of a stock divided by the average earnings of the last 10 years. It’s a better way of showing trend over time. Here is the the Shiller PE ratio going back several decades (courtesy of longtermtrends.net):

The cyclically adjusted price-to-earnings, or CAPE, ratio for the S&P 500 hit 33.1 in November, above the 32.6 level it was at in September 1929, the month before the crash that preceded the Great Depression.

“The fact that we’re beyond the September 1929 levels is obviously an important milestone, and will only add to concerns that current US equity valuations have become disconnected from real economic performance,” Jim Reid, a research strategist with Deutsche Bank, wrote in a note.

To be fair, the article also chalks some of the frothiness “was dismissed by some equity analysts due to the uncertainty of the coronavirus and its impact on forward guidance from companies.” But there’s no denying P/E ratios — like Tesla — are certainly overvalued.

5. Rise of the Retail Investor

“Early in 1928, the nature of the boom changed. The mass escape into make-believe, so much a part of the true speculative orgy, started in earnest.”

John Kenneth Galbraith

I covered a good portion of the boom of the retail investors in 2020 in my Gamestonk post two weeks ago. As of July 2020, retail investors made up over 20% of the entire stock market, fueled by stimulus checks and unemployment bonuses. This was up from 10% only a year prior. A retail investor is defined as someone who buys and sells stock for themselves and not for an entity, fund, or organization.

Global X published an article in October 2020 called “The Renewed Rise of the Retail Investor” and highlighted a key component of the retail investor boom: leverage.

A growing trend within the retail community is the use of leverage to enhance returns. A Yahoo Finance/Harris poll found that 43% of respondents have used margin, options or both since the beginning of the pandemic.19 Traditionally, investors use margin to enhance the returns of small-gain strategies. But it seems that many inexperienced traders today want to supercharge already highly volatile portfolios, bringing them closer to the gains they desire.

Clients are regularly denied access to margin and options strategies due to their inexperience. This wasn’t the case with Robinhood, where higher-level options access originally required a high risk tolerance profile and a certain number of options trades entered on the platform.20 This progression-based system encouraged traders to increase their options activity while potentially overlooking the education component necessary for responsible use. The firm has since updated their options offering, increasing eligibility requirements and educational content.21

Investing can seem easy for the uninitiated when the market’s surging. This makes sense when all you’ve seen is a strong bull market, punctuated by quick pullbacks, over the last decade or so. In this environment, mistaking luck for skill is easy…

Long story short, there’s a party going on right now in Robinhood with loose credit and unchecked greed from inexperienced traders. This sounds exactly like the Investopedia definition of “euphoria”, which occurs in a bubble environment before ‘smart money’ begins profit-taking. “Caution is thrown to the wind as asset prices skyrocket.” It also reeks of pre-crash 1929, with retail investors taking out loans to buy stocks. Financial Times recently published an articled titled “Investor Anxiety Mounts Over Prospect of Stock Market ‘Bubble'”, noting that the rise of “inexperienced amateurs as a particular concern.”

As the old Wall Street maxim goes, the trader on the street is the last one in and the last one out.

The combination of inexperience, high leverage, and total risk aversion is what usually leads the herd to drive the bubble to the point of popping, usually when the credit runs out. There’s also another big obstacle coming in the next 60 days…

A lot of these ‘newly minted’ retail traders starting buying stocks during 2020’s pandemic lockdown out of boredom and checks coming in from the government. With the surge in the market last year, a lot of the common-name stocks saw profits. Now those same retail traders are going to owe capital gains taxes on any profits realized — and given so many of them were short-term investments (owned one-year or less) they’re taxed at ordinary income rates. With the tax bill for 2020’s investing gains due, traders may have to sell current stocks to pay the tax bill. Given that so many Robinhood traders last year were new to buying stocks, they may not be fully versed on how capital gains tax works, and could be in for a shock.

But it’s not over yet.

For those who lost their job or were furloughed and received the $600 weekly unemployment bonus from the Federal government, those checks are also taxed. For a lot of these pandemic stock traders, huge tax bills could be coming. Some may be aware, others may not. As of May 2020, 20 million Americans were receiving the extra $600 Federal unemployment bonus — most of them on the hook for income tax on money collected. With an unexpected tax bill, a lot of these novice retail investors may look to start selling stocks (taking further short-term profits that will be taxed for 2021) to cover tax bills. Remember, these retail investors currently make up over 20% of the stock market. If a large portion begin to sell to cover taxes, well…

The fuse is lit.

6. Companies Pressured into Debt

Last week Bloomberg noted that companies were being pushed towards taking out more debt due to demand in Junk bonds. In “Junk Buyers Desperate For Debt Are Pressing Companies to Borrow,” the authors call to attention the huge demand for “junk bonds and leveraged debt” that investors want to buy up. Junk bonds are typically considered risky, which is why they pay higher yields (junk bonds are also known as “high yield” bonds). The fact that junk bonds are in such demand means investors are clamoring for high yield or better returns on their investments. This means money managers need to keep issuing new junk bonds to meet demand. And to issue a junk bond, a company needs to borrow money — a shaky company that is at risk to justify the high yield.

This likely means companies that probably shouldn’t be going further into debt are being pressured to go further into debt so money managers can sell their junk bond.

This seems freakishly similar to the housing boom, when banks were offering NINJA (no income, no job verification application) loans just to get the mortgages so they could sell them off. Mortgages were being sold to buyers who were unlikely to afford them, or buyers who already had one or more mortgages on other properties. Cue that other scene in The Big Short:

“I own five houses. And a condo.”

Eventually, risky companies are going to be saddled up with debt payments, and it only takes one or two of them to be unable to make payments and the junk bond is defaulted on.

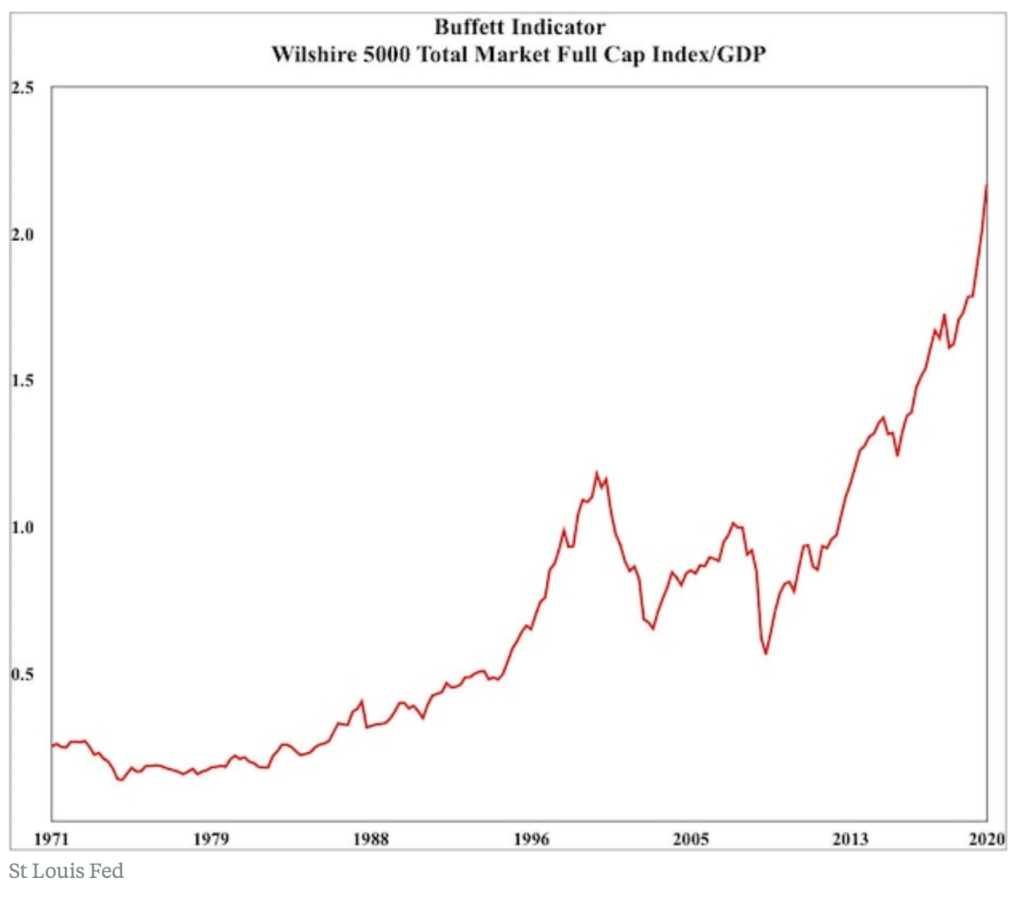

Honorable Mention: The Buffet Indicator

What kind of post would this be if I didn’t mention America’s favorite investor? The ‘Buffet Indicator’ is a ratio favored by Warren Buffet; simply defined as the entire value of the stock market divided by the U.S. Gross Domestic Product (GDP). The idea is to see how the stock market measures in relation to the country’s economy: a ratio of 1 would be a stock market in parity with economy, basically comfortably supported by the products and services of the nation. To measure the ratio, Buffet likes to take the Wilshire 5000 Total Market Index and divided by the most recent quarter GDP number. Buffet himself calls this “probably the single best measure of where valuations stand at any given moment.”

The Buffet Indicator just hit a record high of 195% this past week.

If you look at the chart above, you can see just how far the ratio has pulled away. In the dot com crash of 2000 and the housing bubble of 2007-2008 the indicator isn’t even close where where it is now. The recent parabolic spike comes as no surprise either — lockdowns and COVID-19 have impacted the service and travel industries, reducing the GDP. But the market continued to go up.

“It highlights the remarkable mania we are witnessing in the U.S. equity market,” said Michael O’Rourke, chief market strategist at JonesTrading. “Even if one expected those (Fed) policies to be permanent, which they should not be, it still would not justify paying two times the 25-year average for stocks.”

They don’t Buffet the ‘Oracle of Omaha’ for nothing.

…

I never intended for Quit Your Job to become an investment blog, but investing is a key component to getting out of your soul-crushing 9-to-5 and becoming financially free. Anyone who read my post on Robert Kiyosaki’s Cashflow Quadrant knows the cruciality of the “I” Investor Quadrant. Being an investor means more than buying Apple (AAPL) stock and holding into infinity. You have to know what’s going on in the market, in companies, in economic trends, or you can find yourself wiped out.

And back to the 9-to-5 in no time.

Disclosure: I am not short the market at this time, nor do I have any positions that would benefits from a market drop. I am not a professional investment advisor, nor do I hold any certifications or degrees in finance or economics. I’m just a guy who reads a lot.

Edit: This article was originally published as “5 Signs We’re In a Market Bubble” on February 13, 2021, but after discovering just how high the Buffet Indicator had gotten I wanted to include it in this post. I revised the post from 5 to 6 and added in the BI.

2020 was a rough year. That goes without saying. It was hard to find motivation in writing a blog about Quitting Your Job when so many people were losing their jobs and seeking unemployment assistance. Their jobs quit them. So I watched and waited, trying to find that spark for inspiration to return to the blog-space.

Then came The Big Meme Short.

Because this event is playing out better than any movie that came out in 2020, we’ll take it one step at a time. It will also be partially subjective, because I “took part” so to speak, buying into the market — more for the experience than in any attempt to actually make money. Personally, I believe in investing and do so. I believe in acquiring assets and utilizing dividends (read my post on building a dividend ladder portfolio here). I bought up stocks in April last year and did well. What happened this week was not sane investing and I don’t recommend getting involved (it’s not over as of this writing) and if you do please exercise caution.

That being said: I am not an investing professional or hold any certifications or fancy paperwork that shows I’m a qualified analyst or that you should listen to me. Trade accordingly and consult a financial professional!

Meanwhile, on the other side of the internet, subreddit r/wallstreetbets, essentially a stock trading club of retail investors who discuss stock market strategies, was turning into an angry beehive. It’s worth noting that around the time the GME play got going, the subreddit had about 2.2 million subscribers. It is now up to 5.7 million ‘degenerates.’ Having lost large amounts of money in previous market plays to the big guys on Wall Street, the…shall we say, collective…of wallstreetbets came across the perfect target for revenge.

It involved shorts (I’ll try to keep this brief, but some context is needed). Yes, the same as Burry’s The Big Short. A short is simply a bet against a stock or asset. ‘To short’ something is to bet against. That’s the general term which comes from a ‘short selling’ action where you sell a stock short. An investor on the street can do this by borrowing shares from their brokerage, selling them immediately at market price, collecting the money as profit but owing the brokerage the shares.

Example: I short sell 100 shares of Big Company stock at $10/share. I collect $1,000, but I owe my brokerage (Fidelity, E-Trade, Schwab, etc) 100 shares of Big Company. The stock goes to $5/share, I buy 100 shares of Big Company and return them to the brokerage. I sold for $1,000 and bought back for $500, a difference of $500 which I keep as profit. Brokerage gets their shares back, the trade is over.

Shorting can be dangerous. Imagine if I sold Big Company shares at $10/share and it went to $15/share. Now I’m OUT all the profit AND still owe my brokerage the shares. In most cases, if the trade goes against you, the brokerage will demand their shares back (cause they’re losing money on the value increasing, this is called a margin call). They could also have the power to start selling other stocks in your account to buy back the shares you owe them.

Shorting is a common tactic on Wall Street; it’s done by big banks and hedge funds all the time. The ugly part of it is that with so much weight and money behind it, these funds can actually move the price of stocks in the direction they want them to go. Imagine being able to short Big Company stock and short so much of it it drives the price down in your favor (this is because of volume; when sellers outnumber buyers, the price goes down and vice versa).

So back to r/wallstreetbets. What they discovered was that GameStop (GME) was shorted by Wall Street by over 140%. What does that mean? It means GME stock was heavily bet — the number of shares shorted OUTNUMBERED the amount of available shares. And, if you remember from the example above, the shorted shares must be re-bought to close the position. So, ipso facto, there wasn’t enough shares available to close the position. When the trade was due to close on Friday, January 29, 2021 (last trading day of the month), Melvin Capital, and the other funds behind the short, would need to buy shares to close the short.

As anyone who invests knows, the law of supply and demand rules.

Part One: Short Squeeze

I don’t know when the move to buy up GME started exactly. From the stock chart, the first big move was January 13, where volume spiked and the price rose sharply. For the purposes of this post, we’ll start there.

r/wallstreetbets was at a mere 2.2 million followers or so, but had garnered full buy-in from it’s members on the GameStop play. The price started to climb, more joined in. By the end of last week, I was seeing news about GameStop and ‘short squeeze’ in my news feed, but didn’t bother to look into it.

A ‘short squeeze’ occurs when the price of shorted stock suddenly and sharply rises. In order to ‘stop the bleeding’ (e.g., stop taking losses) a trader or hedge fund will begin to buy the stock back to fulfill the short trade. This, of course, causes the stock to continue to rise because the short seller has started buying too, and it feeds off itself. Stock rises, short seller buys to cover before the price goes up further, which causes the price to rise more, which causes the short seller to buy back more…et cetera.

To use my earlier example of shorting Big Company stock. I borrowed 100 shares and sold at $10, expecting it to go down. Instead, say it goes down to $6 but then starts to come back up. Panicked (and not wanting to lose my profit), I buy 25 shares at $6 — which adds to the increase in price. I still owe my broker 75 shares and the price is rising. So I buy 25 more shares at $8, still owing 50 and my profit is shrinking fast… If it goes to $10, I lose profit on my remaining 50 shares and if it keeps going over $10 I’m losing money. The phenomenon of the price rising against my short and me adding to it is a short squeeze: I’m the one getting squeezed.

I first checked the price of GameStock (GME) on Tuesday at the market open, finding it at about $143/share. My first response was “this is absurd,” the company is in no way worth that. This is a stock that back in October was under $10/share and their business model wasn’t very forward thinking (brick and mortar as games moved online). I checked the stock chart of GME:

At this point, I still had no idea r/wallstreetbets was behind it or what was even going on. From a chart and price perspective, this just looked like a pure mania play. The RSI (relative strength index), the green blob in the top right corner, showed 98+ which means the stock is white hot and severely overbought. My first instinct was to bet against the move using puts.

First: Why bet against it? The reasoning is that it continues to take more money to push a stock price up. Someone (or some fund) must be willing to buy at the current price. In order to sustain huge price gains, there must always be another buyer. The minute no one wants to buy a stock at a certain price, the selloff begins. This is what happened with the dot com crash and any subsequent crash of a stock or market after parabolic moves. I had played a similar trade back in April 2011 in silver:

In late April 2011, silver had climbed to incredibly high levels very quickly. The RSI was high and I knew it couldn’t stay up forever. I bought puts on SLV and within a week the price of silver collapsed. Most money I ever made trading in a day. So, to me, it looked like a similar setup for GME.

I went to make my trade in my Fidelity account but found I wasn’t registered to trade options (my silver play was done in an E-Trade account I’ve since abandoned). I applied, but had to wait at least three days. So, with no trade to make that day, I decided to research exactly what was going on — would I still get a chance to buy puts later in the week? Would the stock mania still be going? So I started to dig.

And I realized something incredible was happening.

Part Two: Can’t Stop. Won’t Stop. GameStop.

It turns out that the story behind GameStop’s ridiculous rise wasn’t the typical ‘rumor mill’ drive up found in past stock manias (remember JDS Uniphase?). It wasn’t a case of “Blue Horseshoe Loves GameStop.” It was a grassroots movement to ‘strike back’ against a faceless enemy in the Wall Street hedge fund. Resentment towards Wall Street for the 2008 housing crash was channeled now into this new play.

What savvy users like /DeepFuckingValue, Roaring Kitty, and r/wallstreetbets discovered was that the big players were extremely exposed on GameStop stock and would be required to buy it at any price. They could create an extremely painful (and expensive) short squeeze against the hedge funds shorting the stock, particularly Melvin Capital. So word was spread, and the degenerates of r/wallstreetstock began to buy GME stock. More importantly, they didn’t just buy — the message was to HOLD.

They would buy up as many shares as they could get their hands on and deny them to the hedge funds. Then they would get their friends, family, and anyone who would listen, to buy and hold too. Because GME was shorted over 140%, more shares were needed to cover than were available, so denying ANY shares further would make things exponentially more painful. Supply and Demand was on full display as GME price rose.

As the price climbed, the redditors’ strategy appeared validated. The truth is, it was a smart play. They caught Melvin with their pants down. Why such a huge short play on GME? I don’t exactly know; GME had a been the target of short plays over the past two years. Maybe Wall Street knew they were a weak target whose stock price could be easily pushed down, particularly with GameStop closing their stores during the pandemic last year. A more insidious theory would suggest Melvin and others wanted to short GME to zero, folding the company and not having to buy back ANY shares, thus keeping 100% of their profit. Regardless, GME’s price was starting to “moon” as it climbed faster.

By Tuesday I noticed the stock and its chart. The grassroots movement was working. Profits garnered interest in what was going on. Interest prompted more buyers — but for the redditors it wasn’t necessarily to get rich, it was to be part of the experience. The GME play had gone viral…like a meme. GME was the first “memestock.” The real memes was also appearing.

When the pandemic started in 2020, lockdowns began and people on the street found themselves stuck at home, receiving stimulus checks and $600 Federal unemployment bonuses. With nothing else to do and/or no work, many took to the retail trading platforms Robinhood and M1 Finance. According to the NY Times, in the first three months of 2020, Robinhood “users traded nine times as many shares as E-Trade customers, and 40 times as many as Charles Schwab customers,” and according to CNBC, retail brokers in 2020 saw “record new account openings…despite the pandemic.” Credit where credit is due: Robinhood and M1 Finance and their $0 commission fee for trading helped force other larger brokers to compete, like Charles Schwab and Fidelity, and drop their commission to $0 as well.

These new retail investors moved like a swarm in 2020, charging after hot name stocks like Tesla (TSLA). The GameStop phenomenon presented itself as the next big target to buy. r/wallstreetbets (now up to 7 million followers in the second day of writing this post) would soon attract these millions of new street investors to their cause. Together, they pushed GameStop up to dizzying heights.

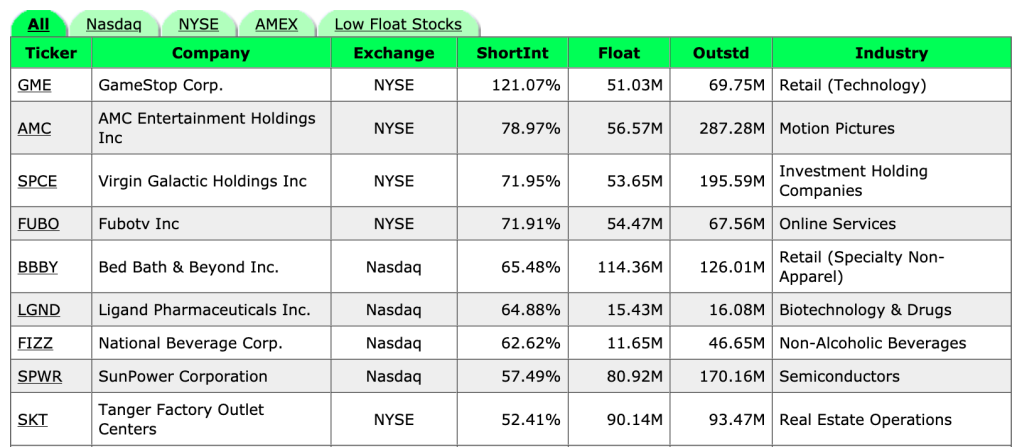

Then something else began to happen. r/wallstreetbets continued to dig and found heavy short positions on other stocks too (just not has hefty as GME). From highshortinterest.com here (as of the end of the week of January 25th) the stocks with the highest short interest (GME lower than the 140% originally, down to 121% which means some shares were bought to cover some of the short):

On Wednesday I decided to enter the fold, just for fun. I had no plans to dive into GME stock head first and my options trading still hadn’t been approved by Fidelity (and still no word). For my own entertainment, I chose AMC stock — I love movies and it seemed an interesting play. It hadn’t rocketed up quite like GME did and maybe it would. I got to play a company related to movie and feel like part of this cultural event.

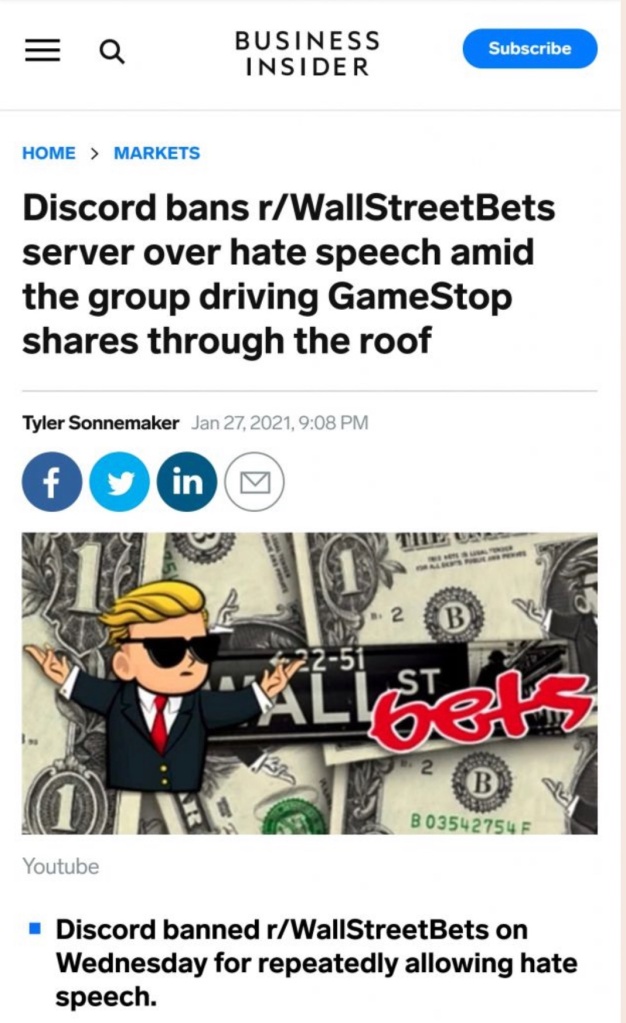

Someone clearly wasn’t happy with r/wallstreetbets. By Wednesday afternoon the subreddit was knocked out of commission, going ‘private’ and not being available to anyone who visited. Even further, the WallStreetBets Discord channel was banned outright. The subreddit would appear public again late Wednesday evening or early Thursday morning, but to this date, the Discord server is still gone. Was this a co-ordinated attack? There’s no doubt at this point WSB was pissing off powers that be.

I would personally experience the coming “fuckery” first hand the following day. It would also validate my original thesis on why GME was a good put choice back on Tuesday (again, before I knew anything about r/wallstreetbets involvement). As if things couldn’t get any wilder, Elon Musk tweeted that day just after market close, driving the price up even more with foreign investors:

Part Three: The House Always Wins…Or Does It?

On Wednesday I was in the game. There were struggles out of the gate; most major brokers were suffering delays in filling orders, likely due to heavy volume. At Tuesday’s close, AMC was just over $6. By pre-market, it had climbed over $12. I was able to finally get my trade through after the bell at 9:30am at $16.50. On Wednesday AMC climbed and closed at $19.90. News came out after the closing bell that Melvin Capital and Citron had exited their short (after getting absolutely leveled). The amount lost by these two hedge funds has varied in the news — Melvin Capital has supposedly lost $7 billion, 53% of their assets under management. GME was over $340/share and the trade was moving in the direction the Redditors planned. Wednesday evening, investing commentary site ZeroHedge reported “Hedge Funds Are Puking Longs to Cover Short-Squeeze Losses.” “Puking longs” means hedge funds are selling long positions to get cash to cover losses incurred due to losses caused by the short squeeze. This is what being margin called looks like.

On Thursday morning, the pre-market price of AMC hit $22. GME was up over $400. Both had been pushed up overnight by foreign traders in India and Europe. North America was getting ready for the next round of the fight when something I’ve never seen before happened.

Brokerages began to restrict only buying not selling. In fact, users were reporting Robinhood (and TD Ameritrade) had REMOVED the buy button for certain equities, namely GME and AMC.

So for all the “meme stocks” (e.g., the heavily shorted stocks pointed out by WSB), Robinhood and TDA were not allowing their users to buy. Promptly, the price on these stocks began to fall. With the retail traders shut out en masse, the sellers would overwhelm the buyers. My shares of AMC were down to $12 when the market opened, wiping out over $7/share in profit. GME price took it on the chin.

Robinhood was claiming they were restricting the stock purchases to protect themselves AND their investors. What it looked like was Robinhood was trying to prevent the dreaded failure to deliver (FTD) that would destroy Robinhood and its capital investors. By failing to deliver, they open themselves up to lawsuits and bankruptcy. By restricting purchases, it helps protect against FTD, but the PR damage was total. RH was a accused of being complicit with the hedge funds to help cover their GME shorts. If retail investors couldn’t buy and only sell, it helped drive down the GME price for the hedge funds to recover. In addition, only being able to sell and not buy might cause panic to the retail investor to get OUT of their Robinhood account, making them hit the “sell” button, thus driving the price lower.

Anyway, at this point I could see the severe shenanigans going on. AMC dropped to the $8 range and I was in the red in my tiny position. I debated just holding and waiting. Then I noticed that every time AMC started to climb back up, the price would halt. Somebody was enacting a trading halt on AMC and GME; I counted no less than 10 halts on the price of AMC before noon alone. Something was happening. After some debate, and the price climbing back to $10/share, I got out. I could have held — I thought about it — but I didn’t like the manipulation and dark forces at work. I took the loss and I’m totally fine with it. It was fun to play and dip my toe into this cultural event.

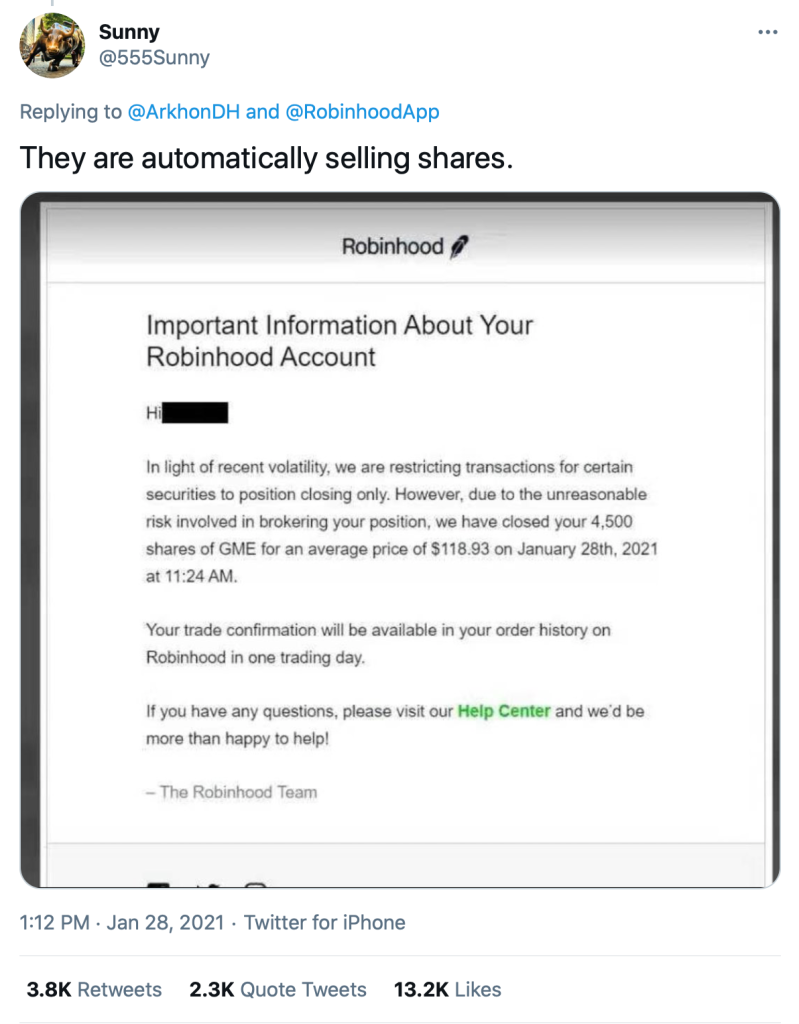

But Robinhood preventing people from buying shares of GME or AMC was only half of the situation. According to several RH users, the app was also selling their GameStock without their permission.Robinhood later denied this had happened, but users took to social media to share screenshots showing the confirmations their accounts had executed sell orders:

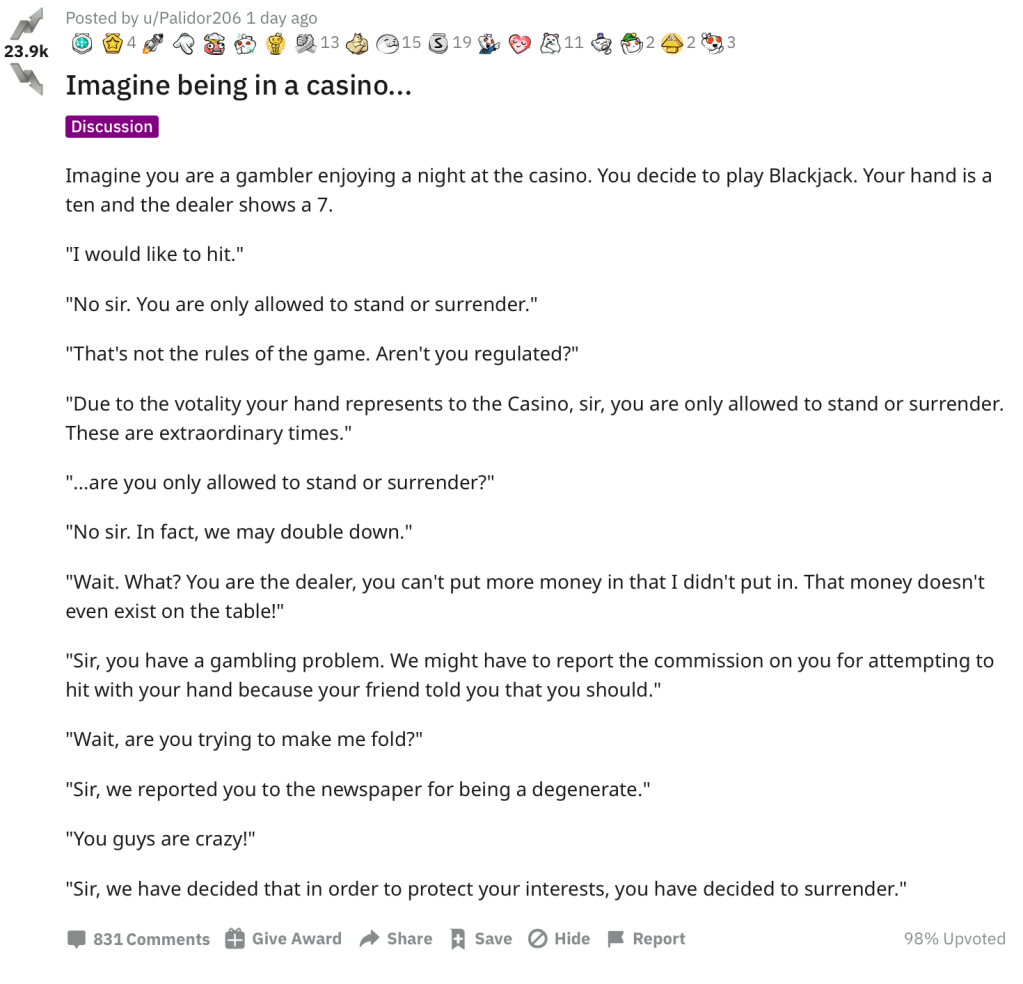

One redditor, Palidor206, described everything happening with Robinhood as such:

And meanwhile…

Part 4: Welcome to Thunderdome

This is a long post, so let’s recap:

Savvy Redditors and a YouTube identified an exploitable play on short sellers of GameStock (GME) shares. They began buying up shares and holding, which encouraged others. The price of GME began to climb.

Early this week GME climbed over $140/share and the number followers of the subreddit r/wallstreetbets exploded. On Wednesday at market open, brokers (including my own, Fidelity) lagged and struggled to keep up with volume.

On Thursday, Robinhood and TD Ameritrade began restricting purchases of the ‘meme stocks’ — GME, AMC, NAKD, BB, NOK, etc. At first the buy button for these stocks was removed; eventually users were restricted to only 1 share. The sell button was always available.

Public backlash at Robinhood exploded, with people protesting and flooding the App Store with 1-star reviews of the app (which Google later removed 100,000 of)

On Friday, although Robinhood restricted purchasing, GME price was back up. AMC was back up (dammit). Nokia (NOK) and BlackBerry (BB) either didn’t have the same force behind them or truly were just a meme as they slid, apparently due to lack of interest.

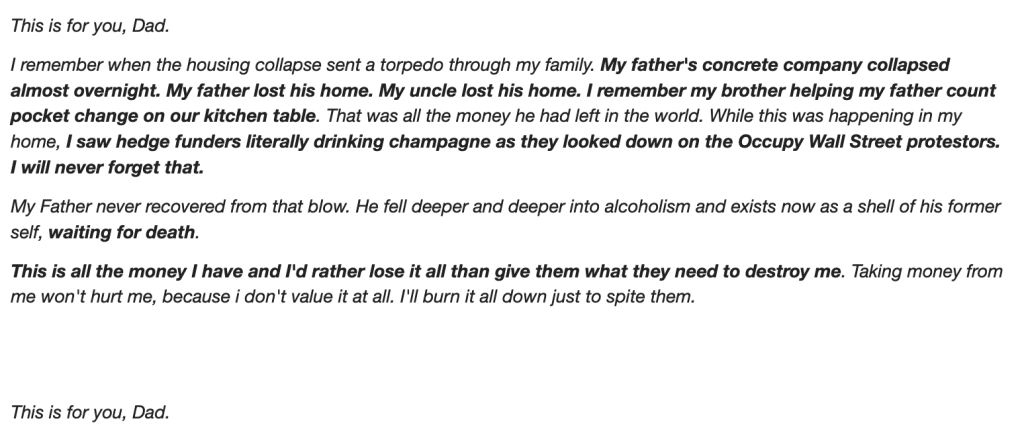

By this point, the emotions behind this retail investor flood went far beyond greed. Followers of r/wallstreetbets began sharing personal stories of why they were doing this. To them, it was personal. They remembered 2008 and what the hedge funds had done to their friends and family. It was payback. Braveheart memes abounded. Perhaps most fascinating about this whole thing was that many of these investors were on suicide missions: it didn’t matter if they made money or if they lost it all. They just wanted to make the hedge funds hurt.

Here’s the story of Space-Peanut on reddit (which has since been removed by a reddit mod, but is available here)

These people don’t care if they lose everything. They don’t care if GME goes to $0. To the reddit investor this is war. They don’t care if it crashes everything down. It’s a new form of populist revolt. As Space-Peanut put it, “Taking money from me won’t hurt me, because I don’t value it at all. I’ll burn it all down just to spite them.”

It’s like being in a gunfight with Doc Holliday — he’s not afraid to take a bullet because you’d just be doing him a favor.

By the way, while writing this, r/wallstreetbets is now up to 7.5 million ‘degenerates.’

The redditors with new found money are now using it to taunt Wall Street publicly.

5. You Are Here

GME is at a mania pitch. The memes are coming hard and fast. There’s reason to think there’s some panic on Wall Street, or at least concern for the chain reaction caused by the Robinhood debacle. See, on Wall Street, everything is interconnected. Brokerages deal with banks and clearing houses. You buy and sell stock in your broker account and it seems instant, but a lot of time it takes days to settle or ‘clear.’ Worst of all, perhaps, is no one knows how deep things can go from one short squeeze.

It’s Sunday afternoon and markets will open in a few hours. What will tomorrow bring? Will GME continue its meteoric rise? Where will the reddit ‘hive-mind’ turn to next? This event with not be without consequence — hedge funds will probably need bailed out. Expect government regulatory commissions and investigations. Will things reach 2008 levels again?

Maybe. Who knows?

WSB has kicked over a rock, exposing what was beneath it. Then they picked up the rock and threw it at a bees’ nest. I expect WSB to be demonized by the media and ‘powers that be.’ These market distortions are they’re fault, after all. If only they had left GME alone this wouldn’t have happened.

What does all this have to do with Quitting Your Job? This blog is certainly not advocating jumping on a bandwagon or chasing the herd for profit. But the biggest takeaway here is the old Boy Scout maxim of “Always Be Prepared.” Weeks ago redditors found a great stock market play. Who knows when the next one will arrive. That also applies in the event the market crashes; if you’re ready, stocks or assets can be bought for cheap while everyone is selling. The other thing I see happening in r/wallstreetbets and Twitter is people on the street becoming interested in financial education — how the stock market works, how stock is traded, what terms mean what. They’re a long way from being savvy, but the interest and desire to learn more is there.

I’m still out on all these meme stocks. But I’m bingewatching the show and it’s fascinating.

Disclaimer: I do not own any of the stocks mentioned in this post. I do not hold GME. I also do not use Robinhood. Caveat emptor.

Uber and Lyft Threaten to Leave California over AB5

Last September I wrote a blog post entitled “California and the Death of the Gig Economy” about California Assembly Bill 5 and the reclassification of contractors as employees. I had my concerns over how companies like Uber and Lyft would react to AB5 and the cost overloads of suddenly having a million new employees added to their balance sheet. Would Uber ramp up automation? Would fares go up? There was also the risk of them up and leaving. So how did it turn out?

Uber and Lyft initially fought back against AB5: The companies, along with DoorDash, filed paperwork in late 2019 for the Protect App-Based Drivers & Services Campaign, a California ballot measure that would create an exemption to AB5 for app-based driver contractors. In 2020, Uber altered its app in an attempt to circumvent the law, letting drives set their own payment rates.

Neither measure worked and this past May California sued the ride-sharing companies to make their contractor drivers into employees. Three days ago, on August 10, 2020, a California judge ruled that Uber and Lyft must comply with AB5 immediately.

So, to recap: A company developed an app and service to bring a lower cost service to consumers. People begin to work for the company to provide said service and were compensated for doing so. The same people now want more, so they go to their state representatives to pass law to force the company to give them more. As California Assemblywoman Lorena Gonzalez put it, “It makes sure that the one million independent contractors in California get the wages and benefits they deserve.”

This was from my blog post last year:

From the first glance here it appears Assembly Bill 5 could have disastrous effects on personal income in the state of California. People working as contractors on their terms will be forced to conform as an employee or lose out on their former gig. Jobs could be lost to automation. Some companies may up and move, taking their jobs with them or choose to cut back because they can’t afford to take on these contractors as employees.

And what happened?

Faced with the massive tidal wave of increased costs for operating in the state of California, Uber and Lyft announced that they’re leaving California. From The Verge:

Lyft said it would shut down operations in California if forced to classify drivers as employees, the company’s executives said in an earnings call with investors on Wednesday. Lyft joins Uber in threatening to pull out of one of its most important US markets over the question of drivers’ employment status…

Both companies have said they would appeal the ruling, which was stayed for 10 days.

But if their appeals fail, Lyft may join Uber in closing up shop in California, the company’s president John Zimmer said. “If our efforts here are not successful it would force us to suspend operations in California,” Zimmer said on a call announcing the second quarter earnings of 2020.

To some, it may look like a grumpy former startup is taking their ball and going home. This article from The Hill has comments full of vitriol toward the “greedy corporations” “extorting” California. Some in the comments call for revoking business licenses for Lyft and Uber — it’s a lot like saying “you can’t quit because you’re fired!”

It’s easy to see why Californians are mad. Scores of Lyft and Uber drivers thought they would suddenly get benefits, paid time off, and a minimum wage are now getting nothing at all if these companies shut down. Don’t forget: these companies have never had a quarter of profit! There’s also the unmentioned damage COVID-19 and the lockdown has done to their businesses. Lyft suffered a 61% revenue drop in the second quarter this year while Uber experienced only a 29% decrease, buoyed by Uber Eats delivery while people were stuck at home.

You can’t get blood from a turnip.

I just don’t see how adhering to AB5 could possibly work at this point. As of March 25, 2020 Uber had about $7 billion in debt (Lyft currently has none). With already not being profitable and suffering corona-related revenue drops, Uber would be forced to borrow more to cover the increased costs associated with converting contractors to employees in California. The choice here is essentially an existential one: Does a company with $7 billion in debt that’s never had a profitable quarter take on more debt to conform to California’s AB5 or do they cut the market loose and spare the debt load? If they take on increased debt to cover 2020’s employee expenses during a pandemic year where they most definitely won’t turn a profit, they’ll have to borrow more again next year to for 2021’s employee costs. They would go deeper into debt with larger debt-servicing payments cutting into yearly expenses against falling revenues.

Even without a current debt load, Lyft would likely have to do the same. After all, these are sudden costs for which money wasn’t previously allocated. Debt would have to be taken on to finance the costs. It becomes existential for Lyft as well. And what if the companies cave to California’s demand and it embolden’s other states to pass their own version of AB5?

The fallout from this will impact millions. All the Uber and Lyft drivers who drive or work for these companies will lose income if the companies shut down (or relocate). To continue to drive for Uber or Lyft these contractors would have to move to a state where they still operate. Less income means less taxes taken in locally and federally from these contractor’s yearly 1099s. This puts California deeper in the current tax revenue hole. Uber — publicly traded as of last year — stock has taken a hit on the ultimatum, reducing the value of retirement accounts and personal brokerage accounts that hold shares.

It will be interesting to see how this plays out, but it does not look good. I wonder if taxi drivers are the only ones celebrating here.

Six weeks into lockdown mode, the U.S. economy is a mess. States are just now starting to open back up, but the damage has been done — some of it permanently. The current unemployment rate in the United States is 14.7% and by some calculations (likely the bureau of labor statistic’s U6 measurement), as high as 23.6%, not far from the peak of the Great Depression.

Bankruptcies are beginning to pile up too. In the month of May alone, Neiman Marcus, Gold’s Gym, and J. Crew have filed for bankruptcy and J.C. Penny is considering it (AMC Theaters possibly too). Wall Street believes the vast majority of the 20 plus million Americans jobs lost will only be temporary — but maybe not so with bankruptcies piling on. Even companies that avoided bankruptcy are slashing jobs at a historic rate: Boeing cut 16,000 jobs in April and, according to a coronavirus layoffs calculator site, 375 startup companies have laid off more than 42,000 employees.

Ok, the point is made. Unemployment is breaking out as a bad as the virus. People are losing their sources of income. Jobs are vanishing — temporary or not.

But there’s something else going on that’s headed straight for the unemployment quagmire.

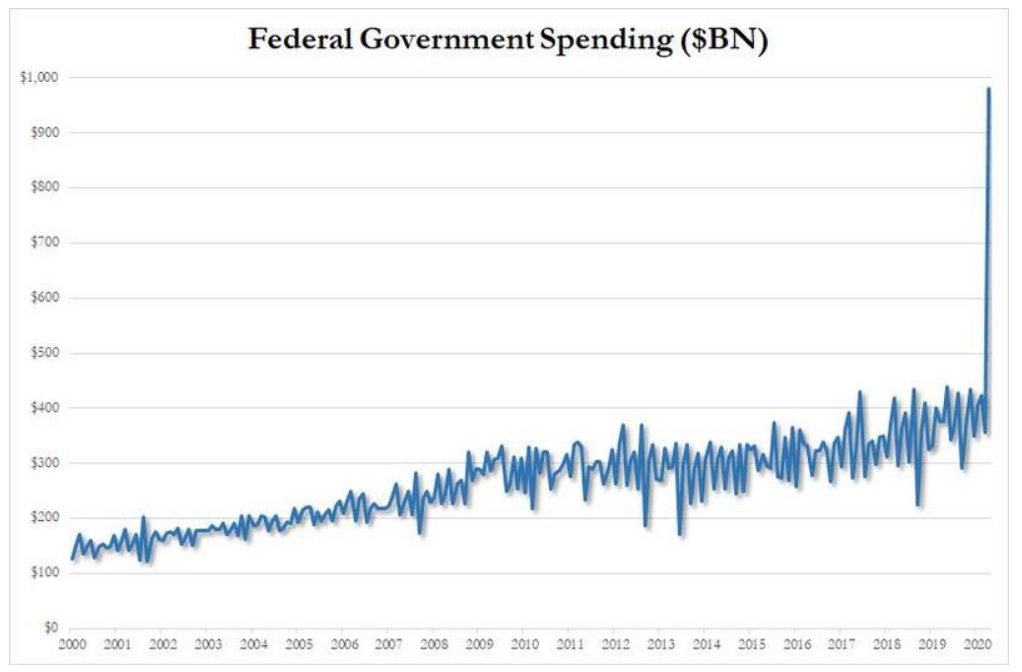

In the six weeks of shutdown due to COVID-19, the Federal Government has spent over $6 trillion. Trillion with a ‘T’. That’s $6,000,000,000,000 — or one trillion dollars per week. $2.4 trillion of that amount comprises four coronavirus relief bills; this includes the CARES Act, SBA Payroll Protection Programs. The remaining money has come directly from the Federal Reserve, who has acted aggressively to stave off economic collapse through numerous programs, including purchasing securities directly. On top of all this, the Fed also reduced bank reserve requirements to zero. This means if you deposit $100 in a bank, they can lend out all $100 of it, keeping none in reserve. This has massive implications — too much to explain here, but watch this to see the impact of reserve requirements in bank lending.

Furthermore, the Fed has also lowered the federal funds rate (the rate banks use to borrow from one another) down near 0%. This rate is used as a benchmark for various other loan rates, reducing the cost of borrowing for mortgages, auto loans, etc. This is the equivalent of turning on the spigot and the handle coming off.

Sure, what’s another $3 trillion on top of the 6 just minted?

In short, there’s more money coming but not necessarily jobs. So what’s the word no one is talking about?

Stagflation.

An odd little portmanteau of “stagnation” and “inflation.” It is a period of high inflation coupled with economic depression. It’s odd too that no one in the media or government is mentioning it, because it looks exactly where we’re heading: $6 trillion and counting in six weeks coupled with job losses and bankruptcies.

Stagnation is a nasty beast because it’s difficult to resolve. In an inflationary environment, rates can be raised to cut off the spigot of currency expansion and reel in spending — a by product is reductions in borrowing and ‘tightening of the belt’ so to speak. Value returns to the currency. In a stagnation — or deflation — prices are falling and money is hard to come by. Loosening the belt allows money to flow a little easier, lending to be encouraged, which leads to businesses expanding via credit (and hiring).

So what do you do when you have falling employment and rising inflation?

If you ‘tighten the belt’ to choke inflation, it worsens the unemployment and makes it even more difficult for businesses to access credit. The currency may level off, but higher interest rates deepen the deflationary hole. If you ‘loosen the belt’ to make credit easier to obtain (e.g., federal funds rate) to save jobs, inflation gets worse prices go up and you risk a total collapse of the currency a la hyperinflation.

The choice is no win, but the effect felt by the average American is even worse. Job loss or cutbacks result in less income. People are left rubbing nickels together and deciding to pay bills or put food on the table. But in a stagflation, prices are rising due to inflation of the currency and suddenly you can’t afford bills OR to put food on the table. You can’t afford anything and there’s no way to bring in more money with the drag on employment.

The last time stagflation hit the United States was in the 1970s. Core inflation (CPI) was over 5% annually during the back half of the 70s, with unemployment high and an official recession running from November 1973 to March 1975. (As a point of reference, the Fed’s federal funds rate during the 70s was mostly between 5% and 10% — it currently is 0.25% to 0%) To choke off the inflation, Federal Reserve Chairman Paul Volcker raised federal funds rate to near 20%, throwing the U.S. into another recession but alleviating the increasing inflation.

I believe Volcker was a rare breed and no one today would pull the trigger on such a hefty interest rate increase. But there was no COVID-19 lockdown in 1979. With unemployment so high, companies going bankrupt or drawing heavily on available credit, jacking interest rates up would shatter all remaining functional pieces of the economy. To wit, another word has surfaced that people are talking about — NIRP.

NIRP stands for Negative Interest Rate Policy. NIRP is the theoretical physics of economics. A negative interest rate works in theory, but suddenly everything goes to plaid. It goes something like this: If an interest rate is 10%, that is the amount it ‘costs’ to borrow money. A loan of $10,000 would cost you a total of $11,000: the original $10,000 principal plus $1,000 (10%) interest. An interest rate of -10% would (in theory) pay you to borrow money. You would borrow $10,000 and get $1,000 for doing so. An $11,000 loan costs you $10,000.

Up is down. Black is white.

This would greatly increase the velocity of money, as banks essentially got paid to take out loans. The problem is, this cuts both ways. Cash deposited at a bank that previously paid interest now costs money. Your $20,000 life savings earning 1% annually now costs you 1% to leave in the bank. Last year your $20,000 became $20,200. This year under negative interest rates it goes from $20,000 to $19,800. You lost $200 by having it in savings.

The concept behind NIRP becomes searingly obvious — borrow and spend. Who in their right mind would save money with negative interest rates? Who wouldn’t borrow when you get paid to do so. In theory, since mortgage rates are tied to the 10-year Treasury yield, but in theory you would pay back less than you borrowed to take out the mortgage.

NIRP would cause everyone to borrow and spend away savings (why keep it in cash losing money when you can invest it or buy something with it?) But how would this impact things like bank profitability when you’re paying people to take out loans? In a NIRP world, home-owners would refinance to try and take advantage of negative rates which would disrupt interest and mortgage-backed bonds. The whole thing is bizarre.

So if the Fed doesn’t crank up interest rates in positive territory, then the only end game here is inflation and prices going up while people struggle to hold or regain jobs. The government can hand out cash in relief packages all it wants to offset jobless and loss of income, but this just further fuels the fire. If this keeps going, a $1,200 stimulus check from the government won’t buy much or things just won’t be affordable at all.

But cutting stimulus checks gives the pretense of ‘doing something’ for the people on the street. Granted, they’re walking a fine line with the COVID lockdown, but spending into infinity is going to be a losing proposition for all. Giving someone a check is simpler than explaining how velocity of money or banking interest rates work.

These germs of disease have taken toll of humanity since the beginning of things–taken toll of our prehuman ancestors since life began here. But by virtue of this natural selection of our kind we have developed resisting power; to no germs do we succumb without a struggle…

H.G. Wells “War of the Worlds”

Updated Edit: I started this post when COVID-19 was first hitting U.S. shores. So much has changed in four weeks and there’s been so much news it’s been a struggle to keep up. However, with each passing day I was increasingly sure the below is true. I intended this to be a much larger article as well, but the deluge of information is going to cause me to break some of the segments out into their own blog posts.

Our world has changed. Not from terrorism. Not from the results of this election year. But from one of the smallest creatures in nature. At less than 50 nanometers in size, COVID-19 proves that even the smallest thing can make the greatest impact. In a few weeks, its presence was felt already on a global scale; here in the U.S., it’s only been the matter of a week and much has changed.

This blog post is important because I feel like we’re at a watershed moment. Just a few weeks ago, the stock market was at its all-time high. Everything felt business-as-normal. We were deep into an election cycle, with non-stop new and critique about the Democratic candidate for President of the United States. There were also still sports.

Now, we’re looking at entirely different country (or even world). It’s starting to feel like a science fiction movie: closed borders and travel bans, closed tourist locations, churches, restaurants, and schools. People have to stay away from each other. The way we work has been forced to change (more on this below). There are also plenty of unintended consequences, mainly economic ones. The U.S. stock market has been decimated; fear runs amok with heavy selling, with days of heavy buying dispersed in between. It’s an economic whipsaw, panic expressed in red and green numbers day in and day out — no one knows whether to buy or sell. Officially, the U.S. stock market has entered a bear market, suffering the fastest 25% drop in history. To many, this feels like the end of the world.

But there’s something interesting here.

This feels like a watershed moment. Things are going to change, regardless of how this plays out. We are living through history at this very moment. Much will be reevaluated in the coming weeks and months and below is just a sample.

Economic Damage

The economic ramifications cannot be downplayed. The U.S. market has suffered heavy selling as people bail out of stocks. Initially, it began as a result of downgrading the outlooks of large companies due to the shutdown of Chinese manufacturing. Factories in China and South Korea have been shuttered for over a month, and are struggling to restart. The length of closing is or will lead to shortages are less product are being manufactured — and many, many global companies rely on them. The disruption of supply chains has led to lower sales, which began pushing stock prices down. Selling begat selling, and then it turned into a rout.

Worse than a battered 401k or fund balance sheet is how the Federal Reserve has reacted. A few weeks ago, the Fed tried to get in front of the selling by cutting the benchmark federal funds lending rate by 50 basis points (bpts). Simply put, lowering the funds rate makes it “cheaper” for banks to borrow money from the Fed (the lending rate is the interest rate banks pay back to the Fed for borrowing; so if the funds rate is 1%, a bank could borrow money from the Fed at 1% and lend it out at 3% and make 2% profit). Last night, on March 15, the Fed lowered the lending rate to the 0% range. This means banks can borrow from the Fed essentially for free. If that weren’t enough, the Fed also fired up a $700 billion quantitative easing program — which it will use to buy up U.S. Treasuries and mortgage-backed securities (remember those?)

In a nutshell, the Federal Reserve is flooding the economy with fresh money to try and stave off recession. Its primary weapon is the federal funds lending rate — which dictates how “expensive” it is to borrow money. This new rate and QE program have effectively made the dollar “cheap,” and could have severe impacts on the value of our currency. In a black hole of selling, deflation sets in — prices drop, cash is in high demand, and businesses penny-pinch. What would could ultimately have is inflation — or hyperinflation — and severely damage our currency’s purchasing power. The U.S. Dollar is the de facto global reserve, with all other currencies pegged to it (there’s not enough time to go into all this now) and ramifications would be global if it suffers in value.